Real Estate Crowdfunding vs Tokenized Real Estate needs your attention!

Real estate investing is no longer limited to buying a whole property or putting money into a public REIT.

Crowdfunding platforms and tokenized real estate platforms have both opened the door to smaller investors.

At first glance, the two models can look similar.

Both allow people to invest smaller amounts into property-related opportunities. Each model can provide exposure to rental income, development projects, or real estate-backed returns. Neither requires the investor to manage a building directly.

The differences matter.

Real estate crowdfunding usually pools investor money into a project, loan, fund, or property deal.

Tokenized real estate uses digital tokens to represent fractional rights linked to an asset, legal entity, income stream, or debt structure.

That may sound like a technical difference, but it affects ownership rights, liquidity, reporting, regulation, and risk.

This guide compares real estate crowdfunding vs tokenized real estate so investors can understand what changes, what stays the same, and what needs checking before any money is invested.

TL;DR — Real Estate Crowdfunding vs Tokenized Real Estate

Real estate crowdfunding pools money from multiple investors into a real estate project, fund, or loan.

Tokenized real estate uses digital tokens to represent fractional rights connected to property, income, debt, or ownership structures.

Crowdfunding can feel simpler for beginners because it often uses familiar online investment platforms.

Tokenized real estate may offer more digital flexibility, but liquidity should never be assumed.

Both models carry property risk, platform risk, regulatory risk, tax risk, and liquidity risk.

Blockchain records can improve ownership tracking, but they do not guarantee strong legal rights or good investment performance.

The best choice depends on the investor’s goals, risk tolerance, time horizon, tax position, and need for access to cash.

Some links in this article may be affiliate links. If you choose to invest through them, we may earn a small commission at no extra cost to you.

This article is for education only. It is not financial, legal, or tax advice.

Quick Answer

Real estate crowdfunding and tokenized real estate both give investors a way to access property without buying an entire building.

Crowdfunding normally works through pooled investment.

A platform raises money from many investors and puts that capital into a property project, real estate loan, fund, or development deal.

Tokenized real estate adds a digital ownership layer.

Instead of only recording investor interests through traditional platform records, tokenized models use blockchain-based tokens to represent fractional rights connected to the underlying asset or legal structure.

The practical difference is this:

Crowdfunding is mainly a fundraising model.

Tokenized real estate is mainly a digital ownership and transfer model.

In real life, the two can overlap. A real estate project could raise money from many investors and also issue tokens. That is why investors need to look beyond labels and read the actual structure.

What Is Real Estate Crowdfunding?

Real estate crowdfunding allows multiple investors to pool money into a real estate opportunity.

That opportunity may involve a rental property, development project, commercial building, fix-and-flip deal, real estate loan, or diversified fund.

The platform usually handles investor onboarding, deal presentation, payment processing, reporting, and updates.

Project sponsors, developers, or asset managers handle the property side.

Investors are usually passive.

They do not choose tenants, manage repairs, negotiate leases, or make daily operating decisions.

Returns may come from rental income, interest payments, profit share, capital appreciation, or a final sale.

The exact structure depends on the offering.

A crowdfunding deal may be equity-based, debt-based, fund-based, or structured through another legal arrangement.

That detail matters because the investor’s rights can change completely depending on the structure.

What Is Tokenized Real Estate?

Tokenized real estate uses digital tokens to represent fractional rights connected to a real estate asset or legal entity.

A token might represent equity in a property-owning company.

Another token may represent income rights from a rental property.

A different structure may represent debt exposure, project finance, or a claim linked to a real estate fund.

The token is not the property itself.

It is a digital representation of rights defined by legal documents.

That point is critical.

A blockchain record may show that an investor holds a token. Legal agreements explain what that token actually means.

For investors, tokenization can make ownership records easier to track. Transfers may also become more efficient if platform rules, regulation, and market demand allow them.

Still, a token does not automatically create liquidity, income, or legal protection.

The structure behind the token matters more than the technology.

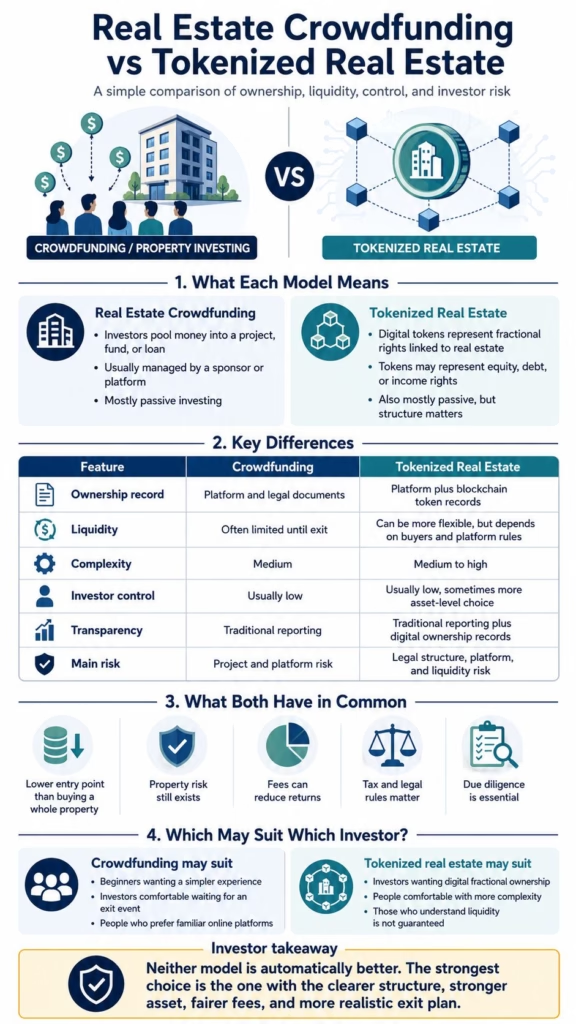

Main Differences at a Glance

| Feature | Real Estate Crowdfunding | Tokenized Real Estate |

|---|---|---|

| Main idea | Many investors pool money into a real estate deal | Digital tokens represent fractional rights linked to real estate |

| Typical structure | Project, fund, loan, SPV, or platform offering | Token linked to equity, debt, income rights, or legal entity |

| Technology layer | Usually traditional online platform records | Blockchain-based token records |

| Investor role | Mostly passive | Mostly passive, sometimes with more asset-level choice |

| Liquidity | Often limited until project exit | Platform-dependent and often limited |

| Transparency | Platform reports and legal documents | Platform reports plus blockchain records |

| Complexity | Medium | Medium to high |

| Best for | Investors wanting simpler online property exposure | Investors comfortable reviewing tokens, platforms, and legal structures |

| Main danger | Illiquidity and sponsor/project risk | Illiquidity, legal complexity, and platform risk |

Neither model is automatically better.

The stronger option is the one with clearer documents, better assets, realistic returns, fair fees, and honest risk disclosures.

Investor.gov explanation of REIT liquidity risks.

Ownership Structure

Ownership is the first area to check.

Crowdfunding investors may own shares in an entity, units in a fund, debt notes, or another contractual interest.

Tokenized real estate investors may hold tokens linked to similar rights.

The label is less important than the legal claim.

A crowdfunding investor might have equity in a property-owning company.

A token holder might have the same type of economic exposure, but represented digitally.

Another investor may only have a claim to income, not direct ownership.

Some deals work more like lending.

Before comparing platforms, investors should ask one basic question:

What do I legally own?

A good platform should answer clearly.

A weak platform hides behind vague terms such as “property-backed,” “asset-linked,” or “blockchain-powered” without explaining the legal rights.

That is not enough.

Liquidity

Liquidity is where tokenized real estate is often oversold.

Many articles claim tokenization creates instant liquidity.

That is lazy.

A token can be easier to transfer than a traditional private real estate interest. Yet selling still depends on buyer demand, platform rules, regulatory restrictions, transfer limits, lockup periods, and market depth.

Crowdfunding deals are often illiquid because investors may need to wait until a project is refinanced, sold, completed, or closed.

Tokenized deals may offer internal marketplaces or secondary trading features.

That sounds better, but the keyword is “may.”

A marketplace with no buyers does not give real liquidity.

For investors, the right approach is simple.

Treat both models as long-term or semi-liquid unless the platform proves otherwise.

Money needed for emergencies should not be placed in either model.

Transparency and Reporting

Tokenised real estate has a potential advantage in transparency.

Blockchain records can show token ownership and transfers.

Smart contracts may also automate parts of income distribution or compliance.

Those features can be useful.

Property investing still needs real-world reporting.

Investors need occupancy updates, rental income, expenses, repairs, valuations, legal documents, tax statements, loan details, and exit plans.

A blockchain record cannot tell you whether a tenant is likely to renew a lease.

It also cannot prove that a property valuation is fair.

Crowdfunding platforms rely more heavily on traditional reporting.

Tokenized platforms may combine traditional reporting with on-chain records.

The stronger model is not the one with the flashier dashboard.

Better transparency means better data, clearer documents, and honest updates when things go wrong.

Investor Control

Both models are mostly passive.

Crowdfunding investors usually have little control after entering a deal.

Sponsors, managers, or platform partners make the main decisions.

Tokenized real estate can sometimes give investors more property-level choice.

For example, investors may choose specific tokenized rental properties rather than a broad pooled fund.

That does not mean they control the property.

Most token holders cannot select tenants, approve repairs, set rents, refinance debt, or force a sale.

Voting rights may exist in some structures, but they are not guaranteed.

Investors should check governance before investing.

Control is not created by owning a token.

Control comes from the legal documents.

Costs and Fees

Fees can quietly damage returns in both models.

Real estate crowdfunding may include platform, sponsor fees, management fees, acquisition fees, development fees, loan fees, servicing fees, and performance fees.

Tokenized real estate may involve similar property-level costs, plus token issuance, transfer, custody fees, blockchain transaction costs, or currency conversion costs.

The important number is not gross yield.

Net return after fees matters.

A deal showing an attractive projected return can become average once all costs are included.

Investors should also check whether fees are taken before or after distributions.

That detail can change the real outcome.

Regulation

Real estate crowdfunding and tokenized real estate often sit inside regulated investment territory.

Rules vary by country.

In the United States, securities-based crowdfunding has specific limits and disclosure requirements.

Tokenized real estate may also involve securities law, property law, digital asset rules, anti-money laundering checks, tax reporting, and transfer restrictions.

Other jurisdictions may treat these structures differently.

Investors should avoid assuming that a platform is safe because it looks professional.

Regulatory language should be clear.

Offering documents should explain who can invest, what rights investors receive, which rules apply, and what restrictions exist.

If a platform avoids these questions, that is a bad sign.

Real Estate Crowdfunding vs Tokenized Real Estate Risk Comparison

Both models carry serious risks.

Property Risk

The underlying asset still matters.

Vacancy, repairs, falling rents, weak demand, bad locations, high insurance costs, and interest-rate changes can damage returns.

Tokenization does not remove normal property risk.

Crowdfunding does not remove it either.

Platform Risk

Investors depend on the platform’s systems, compliance, reporting, payment processing, and support.

If the platform fails, the investor may face delays or confusion.

Strong legal separation between platform operations and investor assets matters.

Sponsor or Manager Risk

The project sponsor, developer, or property manager may perform badly.

Poor management can turn a promising deal into a weak one.

Experience, incentives, track record, and transparency all need checking.

Liquidity Risk

Crowdfunding deals may lock investors in until an exit event.

Tokenized real estate may still lack buyers or face transfer limits.

Both models can be hard to exit early.

Valuation Risk

Private real estate valuations are not always easy to verify.

A platform may show estimated values, but investors need to understand how those figures are calculated.

Optimistic valuations can make returns look better than they are.

Tax Risk

Income may be treated as rent, dividends, interest, capital gains, or something else.

Cross-border platforms can add withholding tax, currency issues, and reporting obligations.

Tax complexity should never be ignored.

Which Model Is Better for Beginners?

Crowdfunding may feel easier for beginners.

The structure is usually familiar: choose a project, invest money, receive updates, wait for income or exit.

Tokenized real estate may require more learning.

Investors need to understand wallets, custody, tokens, legal rights, secondary markets, and platform-specific rules.

That does not make tokenization bad.

It just means beginners should move slowly.

A simple crowdfunding deal with weak terms can be worse than a well-structured tokenized property.

A tokenized deal with poor legal rights can be worse than a traditional real estate fund.

The model matters less than the details.

Beginners should focus on clarity, not novelty.

When Crowdfunding May Make More Sense

Real estate crowdfunding may suit investors who want a simpler online property investment experience.

It may also work better for people who prefer traditional platform records, familiar payment systems, and less technical setup.

Some investors may also prefer crowdfunding when the project sponsor has a strong track record and the legal structure is easy to understand.

The trade-off is usually liquidity.

Crowdfunding investors often need to wait for the project timeline to play out.

That can mean several years.

When Tokenized Real Estate May Make More Sense

Tokenized real estate may suit investors who want fractional exposure with digital ownership records.

It may also appeal to people who are comfortable reviewing blockchain-based platforms, custody options, transfer rules, and token structures.

Asset-level choice can be useful.

A tokenized platform may allow investors to select specific properties, markets, or income profiles.

The trade-off is complexity.

Tokens add another layer to an already complex asset class.

A smooth interface should not distract from the legal documents.

Investor Checklist

Before investing in either model, ask these questions.

Structure Questions

What exactly am I buying?

Is the investment equity, debt, income rights, fund units, or something else?

Which legal entity owns the property?

What rights do investors have?

Can those rights be enforced?

Property Questions

Where is the property?

What type of property is it?

Is it already producing income?

What are the main costs?

How realistic are the projections?

What could cause income to fall?

Platform Questions

Who operates the platform?

How long has it been active?

What happens if the platform closes?

How are investor records stored?

Does the platform publish regular updates?

How does support handle problems?

Liquidity Questions

Can I sell early?

Where would selling happen?

Are there buyers?

Do lockups apply?

What fees apply when exiting?

How long might it take to receive cash?

Tax Questions

What tax documents are provided?

How are distributions classified?

Does foreign tax apply?

Are currency conversions involved?

Should I speak to a tax professional?

Weak answers should stop the investment.

A serious platform should make the basics clear before asking for money.

Market Insight: The Model Is Less Important Than the Structure

Real estate crowdfunding and tokenized real estate are both access models.

They can help smaller investors reach property opportunities that were once harder to enter.

That is useful.

Access alone does not make an investment good.

A weak property remains weak through crowdfunding.

Poor legal rights remain poor when turned into tokens.

Limited liquidity remains a problem even with a digital marketplace.

The best investors look past the headline and study the structure.

That is where the real risk usually sits.

Final Thoughts

Real estate crowdfunding and tokenized real estate both aim to make property investing more accessible.

Crowdfunding is usually easier to understand.

Tokenized real estate may offer more digital flexibility and property-level choice.

Neither model removes the need for due diligence.

Investors still need to check the asset, platform, legal structure, fees, taxes, liquidity, and downside risks.

The strongest approach is not to chase the newest model.

A better approach is to choose the clearest structure, the strongest asset, and the most realistic exit plan.

For beginners, caution beats excitement.

Real estate investing is already complex. Adding crowdfunding or tokenization can improve access, but it can also add new risks.

Understand the model before trusting the opportunity.

Legal Risk Box

Real estate crowdfunding and tokenized real estate may involve securities law, property law, tax rules, digital asset regulation, platform risk, and cross-border investment issues.

Liquidity may be limited in both models.

A token does not automatically guarantee ownership, income, resale access, or investor protection.

Before investing, read the offering documents, understand the legal structure, review the platform’s history, and seek qualified advice where needed.

This article is for informational purposes only and should not be taken as financial, legal, or tax advice.

Frequently Asked Questions

Is real estate crowdfunding the same as tokenized real estate?

No. Real estate crowdfunding pools money from multiple investors into a property deal, fund, or loan. Tokenized real estate uses digital tokens to represent fractional rights linked to property, income, debt, or ownership structures.

Which is more liquid?

Neither model should be treated as highly liquid by default. Tokenized real estate may offer secondary trading in some cases, but liquidity depends on buyer demand, platform rules, regulation, and transfer restrictions.

Is tokenized real estate riskier than crowdfunding?

It depends on the structure. Tokenized real estate can add complexity around custody, tokens, blockchain records, and legal rights. Crowdfunding can also be risky if the project, sponsor, or platform is weak.

Which model is better for beginners?

Crowdfunding may feel simpler because it usually involves fewer technical steps. Tokenized real estate may suit beginners only after they understand tokenization, fractional ownership, legal rights, and liquidity limits.

Can both models generate passive income?

Yes, both may generate income through rent, interest, project returns, or distributions. Income is not guaranteed and depends on the underlying property, costs, fees, and platform rules.

Does blockchain make tokenized real estate safer?

Not by itself. Blockchain can improve ownership tracking, but investor protection depends on the legal structure, platform quality, asset performance, custody, and regulation.

What should investors check first?

Start with the legal structure. Investors need to know what they are buying, who owns the property, how income is paid, what fees apply, and whether they can exit.

Can real estate crowdfunding or tokenized real estate replace owning property?

No. These models can provide property exposure, but they do not provide the same control as direct ownership. Investors usually remain passive and depend on sponsors, platforms, and managers.