Tokenization 2026 turns pilots into production. Banks, funds, and real-asset sponsors move value on programmable rails without ditching compliance.

TL;DR

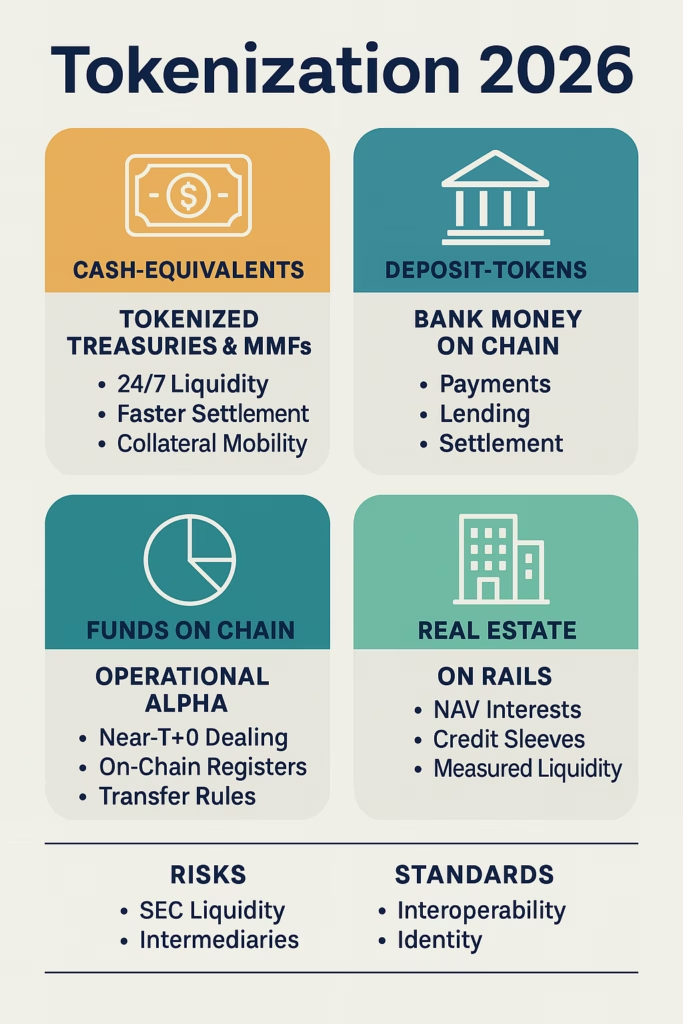

- Tokenization 2026 is the year of usable rails and real workflows.

- Deposit-tokens leave the lab for payments, lending, and settlement.

- Funds on chain deliver near-T+0 dealing, on-chain registers, and transfer controls.

- Treasuries/MMFs and private credit remain cash-equivalent leaders.

- Real estate expands via NAV-based funds and credit sleeves with measured liquidity claims.

- Interoperability, identity, and standards mature across major hubs.

Pull Quote: “Tokenization 2026 is finance with less friction—bank money and assets moving on programmable rails that institutions already understand.”

What “Tokenization 2026” Actually Delivers

Tokenization 2026 is about utility, not novelty. Teams want faster cash cycles, cleaner investor registers, and better collateral mobility—without sacrificing controls. That is why deposit-tokens, fund tokens, and tokenized Treasuries sit at the center. These instruments preserve familiar legal wrappers while gaining programmable benefits. Operations improve without upending risk or governance models. The result is simple: the same assets, on better rails, with better data.

Cash-Equivalents: Treasuries and MMFs

Tokenized Treasuries and money-market shares deliver immediate wins. Treasury teams gain tighter settlement windows, intraday liquidity, and simpler collateral movement. Most flows remain permissioned by design, with selective bridges to public DeFi when controls allow. Through tokenization 2026, expect broader custody links, prime-broker connectivity, and faster subscriptions and redemptions in controlled venues.

Bank Money on Chain: Deposit-Tokens

Deposit-tokens are commercial bank liabilities moving on programmable rails. They interoperate with tokenized securities and fit existing compliance. In tokenization 2026, live use cases appear in marketplace payouts, remortgage steps, and cross-border settlement. The pitch is clear: familiar legal treatment, better auditability, and fewer reconciliations. When cash and assets share standards, everything from payout cycles to collateral calls becomes simpler.

Funds on Chain: Operational Alpha

Fund tokenization updates the plumbing, not the portfolio. On-chain registers, wallet-level restrictions, and near-T+0 dealing reduce friction for managers, distributors, and investors. Under tokenization 2026, more managers adopt transfer-restricted fund shares with on-chain investor records. The asset mix can stay the same. The investor experience and the back office do not.

Real Estate: NAV Interests and Credit Sleeves

Real estate thrives with honest structure. NAV-based interests, income-sharing tokens, and credit sleeves suit tokenization well. Secondary trading remains measured, and that is healthy. Gains show up in digital transfer and registry, transparent reporting, and cleaner secondaries in controlled venues. Tokenization 2026 emphasizes access and operations, not claims of day-trading buildings.

By the Numbers (Credible 2026 Signals)

- Cash/Money instruments: more issuers and better custody/broker rails power 24/7 liquidity parking and quicker collateral turns.

- Private credit: larger, better-tooled conduits and SPVs; on-chain servicing, eligibility controls, and reporting sharpen risk views.

- Funds: Blueprint-style operations roll into production with near-T+0 dealing and on-chain registers.

- Deposit-tokens: multi-bank pilots advance through mid-year in supportive hubs, targeting practical settlement wins.

- Real estate: primary issuance expands with controlled secondaries and standardized registry processes.

How Tokenization 2026 Works (The Stack)

Institutions converge on a practical architecture where money and assets move together on programmable rails. The design is consistent across serious implementations: identity on wallets, rules on transfers, programmable cash for settlement, and pragmatic interoperability.

Identity-Aware Wallets

Investors are verified. Wallets carry eligibility by jurisdiction and investor class. In tokenization 2026, identity moves from a manual checklist to a built-in feature. As a result, compliance becomes continuous, not episodic.

Transfer Rules

Tokens enforce geography, investment limits, resale restrictions, and holding periods at the protocol or application layer. These guardrails lower operational risk and reduce distribution mistakes. Transfers are fast when they should be—and blocked when they should not occur.

Programmable Cash

Deposit-tokens and cash-equivalents such as tokenized T-bills and MMFs support fast settlement, intraday liquidity, and collateral mobility. Tokenization 2026 marries bank money with tokenized assets on consistent rails. The payoff is fewer exceptions, quicker close, and cleaner collateral chains.

Interoperability

Permissioned platforms ship first. Controlled bridges to public chains appear where policy allows. Messaging and standards keep assets mobile enough to be useful and restricted enough to be safe. Therefore, institutions get speed without sacrificing oversight.

Why Tokenization 2026 Matters (Strategic Value)

- Faster value transfer: assets and money move together; settlement is simpler and quicker.

- Operational alpha: on-chain registers and near-T+0 dealing cut overhead, disputes, and errors.

- Better distribution: wallet-level controls reach new segments while safeguarding restrictions.

- Data and reporting: standardized, machine-readable proofs improve risk oversight and attestations.

- Credibility: traditional wrappers persist while the rails become programmable. Stakeholders understand what they own and how it moves.

Implementation Playbook for 2026

Tokenization 2026 rewards teams that pick the right battles and execute.

Treasury & Liquidity Operations

Start with tokenized T-bills and MMFs. You get 24/7 availability, cleaner reconciliation, and faster collateral cycles. Track subscriptions, redemptions, settlement times, and collateral turns in weekly dashboards. Next, integrate with brokers and primes to remove manual steps. Over time, connect these cash equivalents to internal funding pools and margin services.

External reference: BNY Mellon & Goldman’s tokenized MMF operating model illustrates mirror registers and faster dealing cycles (see Goldman GS DAP overview and LiquidityDirect announcements).

Internal link: Your RWA surge explainer — https://tokenizedliving.com/index.php/2025/07/03/rwa-tokenization-surge-2025/

Payments & Lending with Deposit-Tokens

Use deposit-tokens for marketplace payouts, remortgage stages, and cross-border flows. Legal treatment is familiar. Settlement is quick. Audits are simpler. In tokenization 2026, routing cash and securities on the same rails reduces exceptions and delays. Customer support benefits too: fewer breakages, clearer state, and faster issue resolution.

External reference: Bank for International Settlements on tokenised platforms and “unified ledger” arrangements: https://www.bis.org/publ/arpdf/ar2025e3.htm

Funds: Registers, Dealing, and Distribution

Select models that match your distribution channels. On-chain registers cut admin overhead and help transfer agents. Near-T+0 dealing improves client experience and reduces cash drag. Transfer rules keep distribution compliant by design. With tokenization 2026, your fund looks traditional to the investor, but the engine room runs cleaner and faster.

External reference: UK Financial Conduct Authority — Fund Tokenisation Blueprint & 2025 consultation: https://www.fca.org.uk

Real Estate: Design for Reality

Lead with income participation, NAV units, and fractional credit lines. Build digital transfer and reporting first. Treat secondary liquidity as earned, not assumed. As tokenization 2026 unfolds, controlled venues deepen, property data improves, and standardized modules make issuance repeatable. Sponsors win on transparency and cost, not on hype.

External reference: World Economic Forum’s operating models for tokenization in financial markets.

Internal link: here.

Risks & Constraints (Say This Out Loud)

- Secondary liquidity: issuance grows faster than depth in many verticals. Most venues remain allowlisted. Manage expectations early.

- Regulatory sequencing: deposit-tokens may outpace retail stablecoins in some regions in 2026. The order matters for rollout plans.

- Ops integration: many products mirror legacy books on permissioned ledgers before end-to-end composability arrives. Expect parallel systems.

- Data consistency: standardized reporting and attestations improve, but they remain uneven across issuers. Vet data pipelines before scaling.

External reference: MAS Project Guardian notes on tokenised bank liabilities/transaction banking: https://www.mas.gov.sg/initiatives/Project-Guardian

Regional Lens

- United Kingdom: deposit-token pilots continue; fund tokenization guidance enables “operational alpha” launches with transfer-restricted shares and cleaner registers.

- Singapore & other hubs: cross-border transaction banking and FX pilots mature into services; tokenization 2026 highlights bank-to-bank settlement and wallet-aware controls.

- Global policy: reference designs align around platforms mixing central-bank money, bank deposits, and government bonds with embedded compliance.

External references:

BIS — https://www.bis.org

FCA — https://www.fca.org.uk

WEF — https://www.weforum.org

MAS — https://www.mas.gov.sg

What Success Looks Like by December 2026

- Scale: double-digit growth persists in Treasuries/MMFs and private credit issuance.

- Utility: tokenized assets support daily treasury, collateral, and payments—not just demos.

- Policy fit: live experiments inform permanent rule-sets; institutions standardize around identity and transfer rules.

- Credibility: marketing matches market structure. Liquidity is explained, not assumed. Teams speak in workflows, not slogans.

Final thought

For 2026, skip the hype and show the plumbing: bank money that moves like software, funds that operate faster and cleaner, and real assets wrapped in structures investors understand. That story is big enough—and it’s happening.

FAQs: Tokenization 2026

Q1: What is tokenization 2026 in simple terms?

A: The shift from pilots to practical use—money and assets move on programmable, compliant rails that speed routine finance.

Q2: Where will adoption be most visible?

A: Cash-equivalents, deposit-token payments and settlement, and fund operations with on-chain registers and faster dealing.

Q3: Will everything be liquid in 2026?

A: No. Primary issuance grows fast, but open secondary depth is measured. Many assets trade in controlled venues by design.

Q4: How do deposit-tokens differ from stablecoins?

A: Deposit-tokens are bank liabilities that fit existing oversight and interoperate naturally with tokenized securities.

Q5: What should a treasury team do first?

A: Use tokenized T-bills or MMFs. They deliver immediate utility with familiar risk profiles and smooth integrations.

🔮 What’s next?

- Real estate on rails — NAV interests, income sharing, and realistic liquidity.

- Deposit-tokens vs stablecoins in 2026 — what changes for payments, policy, and risk.

- Funds on chain — near-T+0 dealing, on-chain registers, and how managers roll this out.