Tokenized real estate is not limited to rental houses or apartment buildings.

Japan has already tested a more unusual model: a tokenized hotel.

The Sapporo case matters because it shows how real estate security tokens can connect property investing, regulated financial infrastructure, and small investor perks.

At first, that sounds like a simple innovation story.

Look closer, though, and the case becomes more useful.

A hotel is not just a property. It is also an operating business. Room rates, occupancy, tourism demand, staffing, maintenance, and guest experience all affect performance.

That makes a tokenized hotel very different from a tokenized rental home.

This article explains the Kenedix Sapporo hotel case, how Progmat fits into Japan’s security token market, why the utility token angle was interesting, and what investors should check before trusting similar projects.

TL;DR — Tokenized Hotel in Japan

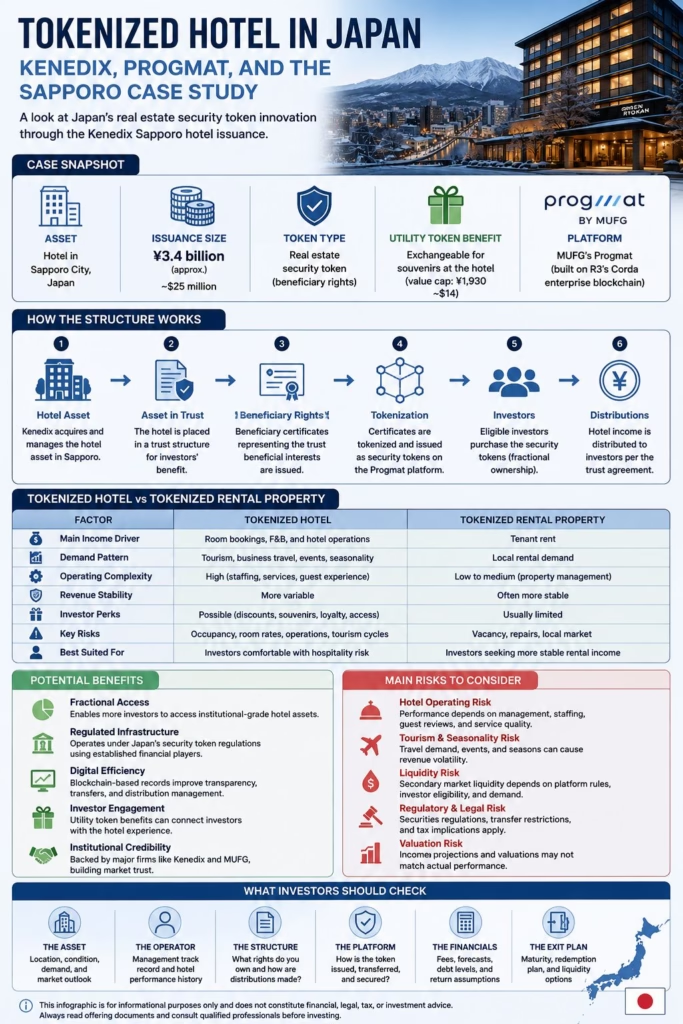

Kenedix used Japan’s real estate security token market to issue a tokenized hotel product linked to a Sapporo City hotel.

The structure used MUFG’s Progmat platform, one of Japan’s major digital securities platforms.

The hotel token included a small utility token benefit that investors could exchange for souvenirs at the hotel.

That perk was not the main investment case, but it showed how hospitality assets can connect investor rights with guest experiences.

Hotel-backed security tokens differ from tokenized rental homes because hotel income depends on occupancy, room rates, tourism cycles, operations, and management quality.

Japan’s security token market has grown quickly, with real estate playing a major role.

Investors should check the legal structure, asset quality, operator, liquidity rules, fees, tax treatment, and platform risk before considering tokenized hotel real estate.

This article is for education only. It is not financial, legal, tax, or investment advice.

What Happened in Sapporo?

Kenedix, a major Japanese real estate asset manager, issued a real estate security token linked to a hotel in Sapporo City.

The offering used MUFG’s Progmat platform.

Reports placed the issuance value at around ¥3.4 billion, which made it a meaningful example of Japan’s real estate security token market rather than a tiny experiment.

The underlying hotel asset supported the security token structure.

Investors did not simply buy a “hotel coin.” Instead, the product sat inside Japan’s regulated security token environment, where real estate-backed rights can move through digital securities infrastructure.

That difference matters.

A casual crypto token and a security token are not the same thing.

Security tokens connect digital records with legal rights, regulated issuance, transfer rules, investor eligibility, and disclosure requirements.

The Sapporo hotel case belongs in that second category.

For readers who want the wider background, our guide to real estate tokenization explains how property rights can be represented through digital investment structures.

Why the Utility Token Was Interesting

The unusual part of the Sapporo hotel case was the utility token benefit.

Investors received a small hotel-related perk that they could exchange for souvenirs at the hotel, up to a capped value.

That detail sounds minor.

Still, it points to a bigger idea.

Hospitality assets can give investors more than financial exposure. They can also create experiences, discounts, loyalty benefits, access rights, or member-style perks.

A rental house cannot easily do that.

A hotel, resort, golf club, or serviced apartment can.

The souvenir benefit did not change the core investment risk. It also did not make the token automatically more valuable.

Even so, it showed how tokenized hospitality real estate can blend investment structure with customer engagement.

For hotels, that could become useful.

A security token can raise capital. A utility benefit can encourage investors to visit, spend, and build a closer relationship with the asset.

That is the real lesson.

How the Structure Worked

The Sapporo hotel token used a real estate security token structure.

In Japan, many real estate security token offerings involve trust beneficiary rights or similar legal arrangements connected to property assets.

The hotel asset sits inside a legal and financial structure.

Digital securities then represent investor rights connected to that structure.

Progmat provides part of the digital securities infrastructure.

This setup differs from a simple platform where users buy informal fractional interests.

A regulated security token structure needs legal documentation, custody, investor records, compliance rules, transfer restrictions, and distribution procedures.

The blockchain layer supports record-keeping and transfer management.

Legal documents still define investor rights.

That point needs repeating in plain English:

The token does not create the investment by itself.

The legal structure gives the token meaning.

If you are new to the concept, start with what tokenization means before comparing different real estate security token models.

Why Progmat Matters

Progmat has become one of Japan’s important security token platforms.

MUFG originally developed the platform, and Japan’s security token ecosystem has used it for real estate-related issuance.

That gives the Sapporo hotel case a wider meaning.

This was not a random property token launched by an unknown startup.

A major Japanese real estate asset manager used institutional digital securities infrastructure to tokenize a hotel-backed investment.

That says something about Japan’s direction.

The country has not treated real estate tokenization only as a crypto-native idea. Instead, large financial institutions, trust banks, brokerages, and property managers have helped build a more regulated market.

For investors, that institutional involvement can improve trust.

However, it does not remove risk.

A serious platform can still host an asset with weak economics. Strong infrastructure cannot make a bad hotel perform well.

Investors need to study both layers: the platform and the property.

Why Japan Matters in Security Tokens

Japan has become one of the more interesting markets for real estate security tokens.

Several reasons explain this.

First, the country has large real estate assets and mature financial institutions.

Second, security token infrastructure has developed through regulated channels rather than only through crypto exchanges.

Third, real estate fits the security token model because property-backed investment products can benefit from fractional access, digital records, and more efficient distribution.

Fourth, Japanese investors already understand REITs and real estate-related financial products.

Security tokens can therefore sit near existing capital market habits, rather than appearing as a completely alien product.

Market reports from Japan also show meaningful growth in security token issuance.

That broader trend makes the Sapporo hotel case more than a one-off headline.

It forms part of a larger movement toward digitized private-market and real estate-backed securities.

It also connects with the wider rise of tokenized resort real estate, where hotels, resorts, and hospitality assets are being tested as digital securities.

Tokenized Hotel vs Tokenized Rental Property

A tokenized hotel and a tokenized rental house may both sit under the “real estate tokenization” label.

The risk profile can differ sharply.

| Feature | Tokenized rental property | Tokenized hotel |

|---|---|---|

| Main income driver | Tenant rent | Guest bookings and hotel revenue |

| Operating complexity | Lower to medium | High |

| Demand pattern | Local rental demand | Tourism, business travel, events, seasonality |

| Management needs | Property management | Full hotel operations |

| Revenue stability | Often lease-based | More variable |

| Investor perks | Usually limited | Possible guest benefits or utility perks |

| Key risks | Vacancy, repairs, local market | Occupancy, room rates, staffing, reviews, tourism cycles |

| Liquidity | Platform-dependent | Securities market and platform-dependent |

This comparison matters because many readers treat tokenized real estate as one simple category.

That is a mistake.

A hotel token, rental home token, office token, debt token, and resort security can all behave differently.

The property type still matters.

The token wrapper only changes how investors access the asset.

For a broader investment-model comparison, our guide to real estate crowdfunding vs tokenized real estate explains how pooled property deals differ from token-based real estate structures.

Potential Benefits of Tokenized Hotels

Tokenized hotel real estate may offer several benefits when the structure works properly.

Fractional Access

Hotels usually require large amounts of capital.

A security token structure may allow investors to gain exposure to hospitality real estate without buying or financing an entire property.

That can broaden access, especially when offerings use regulated securities channels.

Digital Ownership Records

Security token infrastructure can make investor records easier to manage.

That may help with transfers, compliance checks, distributions, and reporting.

Cleaner records matter when many investors participate in one property-backed product.

Investor Engagement

Hotels can offer perks in a way many real estate assets cannot.

A utility token, discount, souvenir benefit, member perk, or loyalty feature can connect investors with the property experience.

That does not replace financial performance.

Still, it can support brand engagement and create a more tangible link between investor and asset.

Institutional Infrastructure

The Sapporo case used Progmat, which gives the article a different tone from many crypto-native tokenization projects.

Institutional infrastructure may help with compliance, investor trust, and market development.

Investors should still avoid blind confidence.

Strong names improve credibility, but due diligence remains essential.

Main Risks Investors Should Understand

Hotel-backed security tokens carry serious risks.

Hotel Operating Risk

A hotel needs guests.

Occupancy, room rates, booking platforms, staffing, food and beverage operations, maintenance, guest reviews, and local competition all affect performance.

Weak operations can damage returns.

A token cannot fix a badly run hotel.

Tourism and Seasonality Risk

Hotels often depend on travel patterns.

Sapporo has seasonal tourism, domestic travel demand, events, weather-related patterns, and regional competition.

A downturn in tourism can reduce revenue.

External shocks can also hit hospitality harder than long-term rental housing.

Liquidity Risk

Security tokens may offer more efficient transfer systems.

That does not guarantee easy resale.

Trading depends on platform access, investor eligibility, regulation, buyer demand, and market depth.

Investors should treat tokenized hotel products as potentially illiquid unless the offering proves otherwise.

Valuation Risk

Hotel valuation can rely on current income, projected occupancy, future room rates, operating margins, and comparable asset sales.

Optimistic projections can make an investment look better than it really is.

Investors should ask how the asset valuation was calculated.

Legal and Regulatory Risk

Security tokens sit inside securities rules.

Those rules can affect who can buy, who can sell, how transfers happen, and what disclosures must appear.

Cross-border investors may face extra tax and legal complexity.

Platform Risk

Progmat and related infrastructure handle digital securities functions, but investors still need to understand custody, transfer process, platform roles, and record-keeping.

Infrastructure matters.

So does the issuer, trustee, asset manager, and distributor.

What Investors Should Check

Before investing in any tokenized hotel product, use a structured checklist.

Asset Questions

Where is the hotel?

Who owns the asset?

How old is the property?

What condition is it in?

Which market does it serve?

How strong is local demand?

What makes the location attractive?

Operating Questions

Who manages the hotel?

What is the occupancy history?

How do room rates compare with local competitors?

Which costs affect margins most?

Does seasonality create large swings?

What happens during weak travel periods?

Structure Questions

What does the security token represent?

Does the investor hold equity, trust beneficiary rights, debt, revenue rights, or another claim?

Who controls distributions?

Which documents define investor rights?

Can investors vote on anything?

What restrictions apply to resale?

Platform Questions

Which platform handles issuance?

How are investor records maintained?

Can the token trade later?

What compliance checks apply?

Who provides custody?

What happens if the platform changes or closes?

Financial Questions

What fees apply?

How does the issuer calculate returns?

What assumptions support the forecast?

How much debt sits against the asset?

When might investors receive distributions?

What exit plan does the issuer expect?

Weak answers should stop the investment.

A hotel token needs more diligence than a catchy headline.

Why the Utility Token Should Not Distract Investors

The utility token feature made the Sapporo case memorable.

Investors should still keep it in perspective.

A souvenir benefit worth a small capped amount does not decide investment quality.

The real questions involve the hotel asset, legal structure, expected income, fees, liquidity, and resale rules.

Perks can help with engagement.

They should not drive the investment decision.

This matters because future tokenized hotel or resort projects may use more creative benefits.

Some might offer discounts, room upgrades, loyalty access, event invitations, or member experiences.

Those features may create value for certain investors.

Yet none of them replace proper investment analysis.

A weak deal with nice perks remains a weak deal.

Market Insight: Hospitality Is a Harder Tokenization Test

The Sapporo hotel case shows tokenization moving into more complex real estate.

That is important for the wider real-world asset market.

Rental properties are relatively easy for beginners to understand.

Hotels require deeper analysis.

A tokenized hotel combines real estate, securities law, tourism economics, hospitality management, and digital asset infrastructure.

That combination may attract institutions and experienced investors.

For beginners, it raises the difficulty level.

More access can help.

Rising complexity creates real danger.

Investors should not treat a hotel token as a simple property share.

They should treat it as a private-market hospitality investment delivered through digital securities infrastructure.

That mindset is safer.

That matters because real-world assets now include more than simple property tokens, with hotels, debt products, funds, commodities, and infrastructure also entering the market.

Not always. Liquidity depends on platform rules, securities restrictions, buyer demand, eligibility checks, and market depth.

Final Thoughts

The Kenedix Sapporo hotel case gives investors a useful window into Japan’s security token market.

It shows how a real estate asset manager can use regulated digital securities infrastructure to tokenize hotel-backed investment rights.

The small utility token benefit added another layer by connecting investors with the hotel experience.

That makes the case interesting.

It does not make tokenized hotel real estate simple.

Hospitality assets carry operating risk, tourism risk, valuation risk, liquidity limits, and legal complexity.

Progmat and Japan’s security token market provide stronger infrastructure than many speculative crypto projects, but infrastructure alone does not guarantee returns.

The asset still comes first.

The legal structure comes second.

The token comes third.

Investors who remember that order will make better decisions.

Legal Risk Box

Tokenized hotel investments may involve securities law, trust structures, property law, tax rules, custody arrangements, platform risk, and resale restrictions.

Hotel-backed assets also carry operating risk, tourism risk, seasonality, valuation uncertainty, and liquidity limits.

A token does not guarantee income, resale access, investor protection, or property performance.

Before investing, read the offering documents, review the hotel asset, understand the legal structure, check the platform rules, and speak with qualified professionals where needed.

This article is for informational purposes only and should not be taken as financial, legal, tax, or investment advice.

Frequently Asked Questions

What is a tokenized hotel?

A tokenized hotel uses digital securities or tokens to represent investment rights linked to a hotel asset or hotel-related legal structure.

What happened in the Kenedix Sapporo case?

Kenedix issued a real estate security token linked to a Sapporo City hotel using MUFG’s Progmat platform. Reports placed the issuance value at around ¥3.4 billion.

What made the Sapporo hotel token unusual?

The structure included a small utility token benefit that investors could exchange for hotel souvenirs. That perk linked the investment product with the hotel experience.

Is a tokenized hotel the same as a tokenized rental property?

No. A rental property usually depends on tenant rent. A hotel depends on occupancy, room rates, tourism demand, staffing, management quality, and guest experience.

Does tokenization make hotel investing safer?

No. Tokenization can improve digital records and access, but it does not remove hotel operating risk, valuation risk, legal complexity, or liquidity limits.

Can investors sell tokenized hotel securities easily?

Why does Progmat matter?

Progmat provides digital securities infrastructure in Japan. Its role matters because the Sapporo case used regulated security token infrastructure rather than a casual crypto token model.

What should investors check first?

Start with the legal structure, asset quality, hotel operator, fees, expected income, resale rules, and platform documentation.