Most people discuss tokenized real estate through rental homes, apartments, or commercial buildings.

Hospitality real estate is different.

A hotel or resort is not just a building. It is an operating business, a property asset, a guest experience, and a management challenge all at once.

That makes the Tuscany National Resort and Club case useful.

It shows how tokenized securities may be used in hospitality real estate, especially for large projects that would normally sit outside the reach of most investors.

The idea sounds exciting, but it also needs a serious risk check.

Tokenizing a luxury resort does not remove development risk, operating risk, liquidity risk, regulation, or the challenge of actually running a profitable hospitality business.

This case study explains what happened, why it matters, and what investors should learn from it.

TL;DR — Tokenized Resort Real Estate

Tokenized resort real estate uses digital securities or tokens to represent investment rights linked to a hotel, resort, or hospitality project.

The Tuscany National Resort and Club case involved a luxury resort project in Cortona, Italy.

The project was linked to tokenized securities and later a $20 million Reg D capital raise using the tZERO Securities platform.

Hospitality real estate is more complex than simple rental property because returns depend on occupancy, tourism demand, operations, seasonality, staffing, and guest experience.

Tokenization may improve access and digital record-keeping, but it does not guarantee liquidity or profits.

Investors must understand the legal structure, offering terms, project stage, operator experience, fees, exit plan, and securities rules.

This article is for education only. It is not financial, legal, tax, or investment advice.

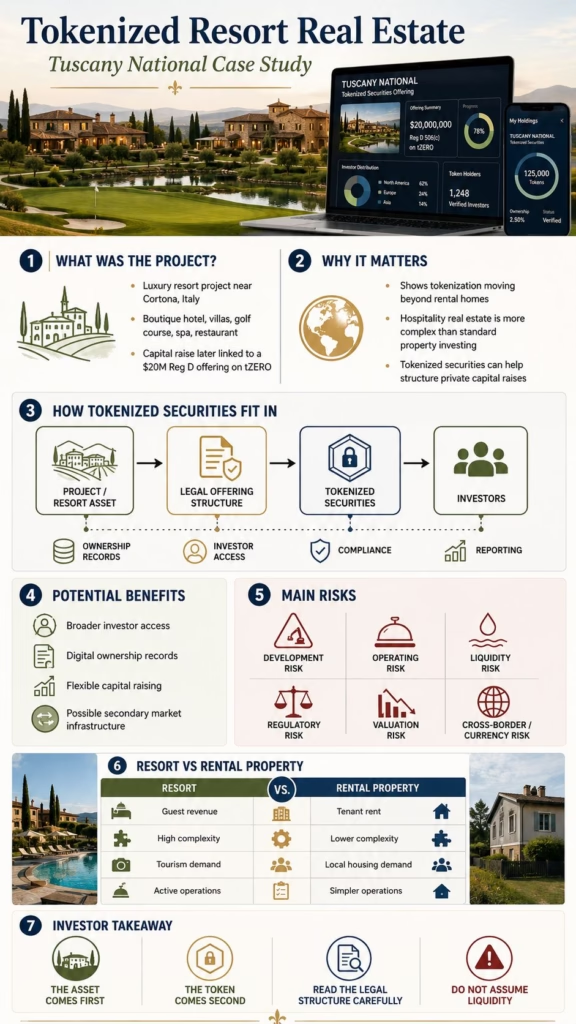

What Was the Tuscany National Resort Project?

The project team presented Tuscany National Resort and Club as a luxury hospitality real estate project near Cortona, Italy.

Project materials described the resort as including a boutique hotel, villas, a golf course, restaurant, spa, and related hospitality facilities.

In 2023, Valhil Advisors announced that it would advise Park Street Development Group and Buena Vista Hospitality Group on the issuance of tokenized securities for the project.

A later 2024 update said Park Street Tuscany, LLC launched a $20 million Regulation D capital raise through the tZERO Securities platform.

That later update described the asset as a 200-acre property in the Tuscan region, with a 47-room boutique hotel, 24 VIP villas, an 18-hole Gary Player-designed golf course, a full-service restaurant, and a spa.

So the story is not just “a resort using blockchain.”

The more useful angle is this:

A hospitality real estate project used tokenized securities infrastructure as part of its capital-raising strategy.

That distinction matters.

Why This Case Study Matters

Most tokenized real estate platforms focus on residential rental properties.

Those assets are easier to understand.

A house has tenants. Rent comes in. Costs go out. Investors may receive distributions if the structure allows it.

Hospitality real estate is much more complicated.

A resort depends on nightly rates, occupancy, tourism cycles, staff, management quality, marketing, guest reviews, food and beverage revenue, maintenance, local travel trends, and broader economic conditions.

A beautiful property can still become a poor investment if operations are weak.

That is why this Tuscany case matters.

It shows tokenization moving beyond simple property income and into higher-complexity commercial real estate.

Investors need to understand that jump.

A tokenized resort is not the same as a tokenized rental house.

What Are Tokenized Securities?

Tokenized securities represent investment rights in digital form.

The legal documents may link those rights to equity, debt, revenue share, fund units, or another regulated investment structure.

The token is not the main thing.

The legal documents are the main thing.

A token may show ownership records or make transfers easier. It may also help platforms manage investors, compliance, custody, and reporting.

However, the rights behind the token decide what investors actually own.

In a hospitality project, those rights might relate to a company, project vehicle, debt instrument, or investment contract.

That is why investors must read the offering documents.

A tokenized security is still a security.

Regulation, restrictions, disclosures, resale limits, investor eligibility, and risk warnings all matter.

Regulation D and Accredited Investors

The Tuscany capital raise was described as a Regulation D offering.

That matters because Regulation D offerings are not the same as public stock market investments.

They are private securities offerings that rely on exemptions from full SEC registration.

In many cases, you are limited to accredited investors or investors who meet specific suitability rules.

That can make these offerings very different from retail tokenized real estate platforms.

A beginner should not see “tokenized” and assume open access.

Some tokenized securities are still private-market products.

Private offerings may limit participation to accredited investors and place restrictions on resale.

The investor may need to hold the asset for a long time.

That is not automatically bad.

It just means the investment belongs in the private-market category, not the simple “buy and sell anytime” category.

How Tokenization Can Help Hospitality Real Estate

Tokenization may help hospitality real estate in several ways.

First, it can create a digital investor record.

That may make cap table management, ownership tracking, and compliance easier for the issuer.

Second, tokenization may support fractional access.

Large hospitality projects often require substantial capital. A digital securities structure can allow more investors to participate within the rules of the offering.

Third, platforms may improve distribution and reporting.

Investors can potentially see documents, updates, and ownership records through a digital interface.

Fourth, secondary-market infrastructure may improve exit options over time.

That point needs caution.

A tokenized security is not automatically liquid. Trading depends on platform support, regulatory restrictions, buyer demand, holding periods, and market depth.

Tokenization can create the rails.

It cannot force buyers to appear.

Why Hospitality Real Estate Is Different

Hospitality assets do not behave like ordinary rental homes.

A rental property may have one tenant on a long lease.

A resort needs constant demand.

Guests must choose it again and again.

That creates a different risk profile.

Occupancy can change by season.

Tourism trends can shift.

Airline capacity may affect visitor numbers.

Local competition can pressure room rates.

Food, staffing, utilities, maintenance, insurance, and marketing costs can rise.

A strong brand or operator can help, but execution still matters.

Resorts also require ongoing capital spending.

Rooms need upgrades. Grounds need care. Guest areas must stay attractive. Golf courses require specialist maintenance.

A tokenized structure does not remove any of this.

Hospitality returns come from operations, not just ownership records.

Potential Benefits of Tokenized Resort Securities

Tokenized resort securities may offer several possible benefits.

Broader Access

Hospitality real estate has usually been difficult for smaller investors to access directly.

Tokenized securities may allow qualified investors to participate in deals that were once limited to larger institutions, private equity firms, or wealthy individuals.

That access can be valuable if the structure is clear and the project is strong.

Digital Ownership Records

Digital securities can make ownership tracking cleaner.

This may help issuers manage investors, transfers, records, and reporting.

Good record-keeping matters in private markets, especially when there are many investors.

More Flexible Capital Raising

Project sponsors may use tokenized securities to reach a wider pool of investors.

That can be useful when traditional financing is difficult or expensive.

For development or acquisition projects, alternative capital channels may help move a deal forward.

Possible Secondary Market Access

Some tokenized securities platforms use regulated trading infrastructure.

In theory, that may give investors more exit options than traditional private placements.

In practice, liquidity still depends on rules and demand.

Investors should treat secondary access as a possibility, not a promise.

Main Risks Investors Should Understand

The risks are serious.

Development Risk

If the resort is unfinished, delayed, over budget, or dependent on future approvals, investors carry development risk.

A beautiful project plan does not guarantee completion.

Costs can rise.

Timelines can slip.

Financing can change.

Operating Risk

Hotels and resorts are active businesses.

Poor management can damage revenue.

Weak occupancy can hurt cash flow.

Bad reviews can reduce bookings.

Staffing problems can increase costs.

A token cannot solve operational failure.

Liquidity Risk

Private securities can be difficult to sell.

Tokenization may improve transfer systems, but it does not automatically create a liquid market.

A listed token with few buyers is still illiquid.

Regulatory Risk

Tokenized securities operate inside securities rules.

Transfer restrictions, investor eligibility, compliance checks, and platform rules can limit who can buy or sell.

Cross-border assets add more complexity.

Valuation Risk

Resort valuations can be difficult.

They may depend on projected earnings, comparable sales, tourism growth, development assumptions, and future operating performance.

If projections are too optimistic, investors may overpay.

Currency and Jurisdiction Risk

A project in Italy with investors from other countries may create currency, tax, and legal issues.

Investors need to understand which laws apply and how disputes would be handled.

Tokenized Resort Real Estate vs Tokenized Rental Property

| Feature | Tokenized rental property | Tokenized resort real estate |

|---|---|---|

| Main income source | Rent from tenants | Hospitality revenue from guests |

| Complexity | Lower to medium | High |

| Operating needs | Property management | Full hospitality operations |

| Demand driver | Local rental market | Tourism, occupancy, pricing, brand |

| Risk profile | Vacancy and maintenance | Development, occupancy, staffing, seasonality |

| Investor access | Often retail or platform-based | Often private securities / accredited investor model |

| Liquidity | Platform-dependent | Platform and securities-rule dependent |

This comparison shows why investors should not treat all tokenized real estate as one category.

A rental home, office building, hotel, resort, and development project can all be tokenized.

The token layer may look similar.

The real-world risk can be completely different.

What Investors Should Check

Before considering any tokenized resort deal, investors should ask hard questions.

Project Questions

Is the resort already operating?

If not, what remains to be completed?

What is the development budget?

Who controls construction and operations?

Which permits or approvals are still needed?

What happens if costs rise?

Hospitality Questions

Who will manage the resort?

What is the operator’s track record?

What occupancy rate is assumed?

How realistic are room-rate projections?

How seasonal is demand?

Who are the competitors?

Legal Questions

What does the tokenized security represent?

Is it equity, debt, revenue share, or another claim?

Which entity owns the property?

What rights do investors have?

Can investors vote?

What restrictions apply to resale?

Financial Questions

How will investor money be used?

What fees apply?

How are returns calculated?

What is the exit plan?

Is the valuation based on current performance or future projections?

What happens if the project underperforms?

Platform Questions

Which platform handles the offering?

Is secondary trading available?

Who provides custody?

What compliance checks apply?

How are records maintained?

What investor updates will be published?

Weak answers are not small problems.

In private-market real estate, unclear structure is a major warning sign.

Market Insight: Tokenization Is Moving Up the Complexity Curve

The Tuscany National case shows tokenized real estate moving beyond simple rental property exposure.

That is important.

As tokenization expands, investors will see more complex assets: hotels, resorts, funds, debt products, infrastructure, private credit, and mixed-use developments.

More access can be good.

More complexity can be dangerous.

The investor skill requirement rises as the asset becomes harder to understand.

A tokenized resort deal requires more due diligence than a simple explanation of fractional ownership.

Investors need to understand hospitality economics, private securities, legal structure, liquidity limits, and platform risk.

Tokenization may open the door.

It does not tell investors whether they should walk through it.

Final Thoughts

The Tuscany National Resort and Club case shows how hospitality projects may use tokenized securities.

It shows that tokenization is not limited to small rental homes or simple property platforms.

Resorts, hotels, and other commercial real estate assets may also use digital securities infrastructure to raise capital and manage investor records.

That is the opportunity.

The risk is treating every tokenized asset as if it works the same way.

A luxury resort has very different economics from a residential rental property.

Development timelines, operating performance, tourism demand, management quality, and liquidity all matter.

Tokenized resort real estate may become an important part of the wider real-world asset market.

For now, investors should approach it as a private-market real estate case study, not a guaranteed glimpse of the future.

The asset comes first.

The token comes second.

Legal Risk Box

Tokenized resort real estate may involve securities law, private placement rules, property law, hospitality operations, tax rules, digital asset custody, and cross-border investment issues.

A tokenized security does not guarantee income, liquidity, voting rights, capital appreciation, or investor protection.

Private offerings may limit participation to accredited investors and place restrictions on resale.

Before investing, read the offering documents, understand the legal structure, check the operator’s track record, review the platform rules, and seek qualified advice where needed.

This article is for informational purposes only and should not be taken as financial, legal, tax, or investment advice.

Frequently Asked Questions

What is tokenized resort real estate?

Tokenized resort real estate uses digital securities or tokens to represent investment rights linked to a resort, hotel, or hospitality real estate project.

Was Tuscany National Resort and Club tokenized?

The project was announced as a tokenized securities initiative involving Valhil Advisors, Park Street Development Group, and Buena Vista Hospitality Group. A later update described a $20 million Reg D capital raise using the tZERO Securities platform.

Is tokenized resort real estate the same as tokenized rental property?

No. Rental property usually depends on tenant rent. Resort real estate depends on hospitality operations, occupancy, room rates, tourism demand, staffing, and guest experience.

Can tokenized resort securities be traded?

Possibly, but liquidity should not be assumed. Trading depends on platform rules, securities restrictions, buyer demand, eligibility requirements, and market depth.

Are tokenized hospitality deals open to beginners?

Many tokenized securities offerings may be limited to accredited investors or qualified participants. Beginners should not assume that every tokenized real estate deal is open to retail investors.

What are the biggest risks?

Key risks include development delays, operating performance, illiquidity, valuation assumptions, regulatory restrictions, platform risk, currency issues, and cross-border tax complexity.

Does tokenization make hospitality real estate safer?

No. Tokenization may improve records, access, and transfer systems, but it does not remove hospitality business risk or real estate risk.

What should investors check first?

Start with the legal structure and project status. Investors need to know what the security represents, who owns the asset, how funds are used, who operates the resort, and how exits work.