TL;DR

RWAs stands for real-world assets.

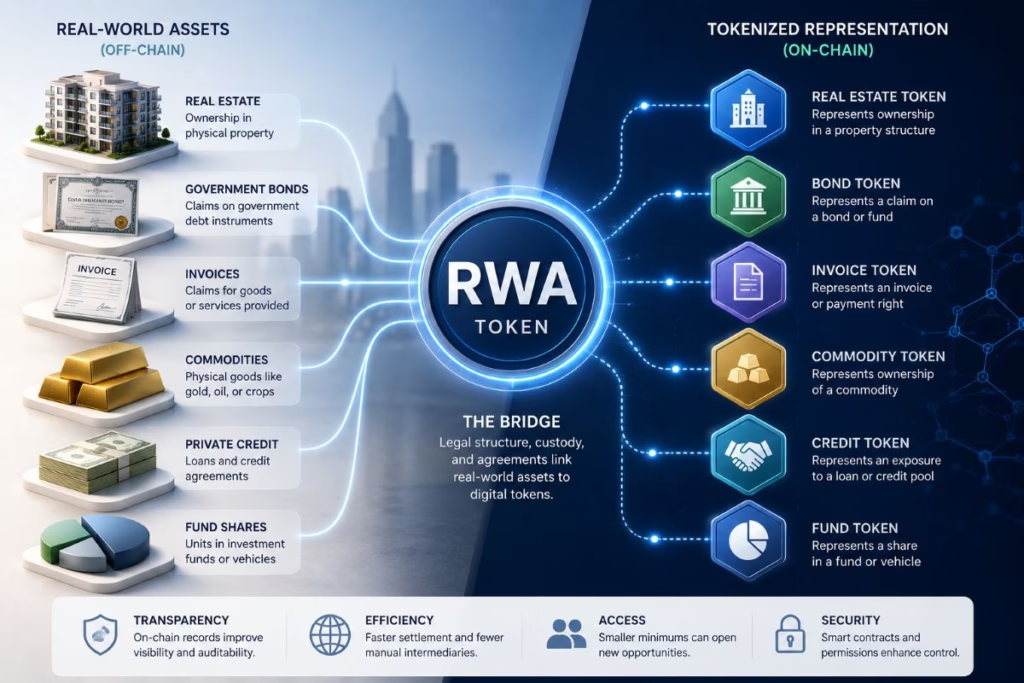

These are assets, rights, or financial claims that exist outside blockchain networks.

Examples include real estate, government bonds, money market funds, private credit, gold, commodities, invoices, art, and fund shares.

When people talk about RWAs in crypto, they usually mean real-world assets represented through digital tokens.

That does not mean the asset itself moves onto a blockchain.

A building stays in the real world.

Gold stays in a vault.

A bond remains a financial instrument.

The token usually represents a right, claim, share, or record linked to that asset.

That difference matters.

Before trusting any RWA product, ask one simple question:

What does this token actually represent?

What Are RWAs?

RWAs are real-world assets.

In simple terms, they are assets from outside the crypto world.

Some are physical, like property, gold, art, or farmland.

Others are financial, such as bonds, money market funds, invoices, private credit, or fund shares.

A loan agreement can also count as an RWA.

So can a company that owns a real estate asset.

The key point is this:

An RWA gets its value from something beyond the blockchain.

Bitcoin is not an RWA.

Ether is not an RWA.

A meme coin is not an RWA.

Those are crypto-native assets.

By contrast, a token linked to a Treasury fund, property structure, carbon credit or gold reserve may sit inside the RWA category.

The token may live on a blockchain.

The asset behind it does not.

RWA Meaning in Crypto

In crypto, RWA usually means a real-world asset that has been represented on-chain.

That sounds technical, but the idea is not hard.

A token may represent rights linked to a real asset.

For example, a tokenized property product might give investors exposure to a building through a company or legal structure.

A tokenized Treasury product may represent shares or units in a fund that holds short-term government securities.

Gold-backed tokens may connect to physical gold held by a custodian.

Those examples all fall under the RWA umbrella.

However, they are not the same type of investment.

One may depend on property management.

Another may depend on fund rules.

A third may depend on custody and redemption rights.

That is why beginners should never stop at the label “RWA.”

The label tells you the asset category.

It does not tell you what you own.

Simple Examples of RWAs

RWAs cover a wide range of assets.

Here are some common examples:

| RWA Type | Simple Example | What Beginners Should Check |

|---|---|---|

| Real estate | Apartments, houses, or commercial buildings | Who owns the deed? |

| Government bonds | U.S. Treasuries or Treasury funds | What structure holds the bonds? |

| Money market funds | Funds holding short-term securities | Who manages the fund? |

| Private credit | Loans or credit pools | Can borrowers repay? |

| Commodities | Gold, silver, oil, or agricultural goods | Who stores and audits the asset? |

| Art and collectibles | Paintings, watches, wine, or cars | How is value proven? |

| Invoices | Business invoices waiting for payment | Who owes the money? |

| Fund shares | Units in an investment fund | What fees and restrictions apply? |

This variety is useful.

It also creates confusion.

A tokenized apartment building and a tokenized Treasury fund may both count as RWAs.

Their risks are completely different.

Real estate involves tenants, repairs, local laws, vacancies, and management.

Treasury products depend more on fund rules, interest rates, custody, and investor access.

Private credit brings borrower risk.

Commodities bring storage and audit questions.

So the smart move is simple:

Do not treat RWAs as one single market.

Compare the structure behind each product.

Why RWAs Matter

RWAs matter because they connect traditional assets with blockchain-based systems.

For years, crypto focused mostly on native digital assets.

That included cryptocurrencies, DeFi tokens, NFTs, stablecoins, and blockchain infrastructure.

RWAs bring a different angle.

They ask whether real-world assets can use blockchain for ownership records, settlement, transfers, compliance, and investor access.

For retail investors, the pitch often centers on access.

A tokenized asset may allow smaller investors to get exposure to property, funds, bonds, or credit products.

Institutions care about something else.

Banks, asset managers, and market infrastructure firms often focus on settlement, collateral movement, reporting, audit trails, and operational efficiency.

Those points sound less exciting than “own a piece of a building.”

In the long run, they may matter more.

RWAs and Tokenization

RWAs and tokenization are closely linked.

An RWA is the real-world asset or financial claim.

Tokenization is the process used to represent it digitally.

Here is the clean version:

RWAs are the assets.

Tokenization is the digital method used to represent rights linked to them.

A property is an RWA.

A token linked to a property-owning company may be a tokenized RWA.

A Treasury fund can be an RWA product.

A blockchain-based share or unit of that fund may be a tokenized asset.

Gold held in custody is a real-world asset.

A token that represents a claim linked to that gold may be part of the RWA market.

The token is not the full story.

It is only the front end.

The real question is what sits behind it.

What Does an RWA Token Represent?

An RWA token can represent different things.

It may represent:

- A share in a fund

- An interest in a company

- A claim on income

- Debt exposure

- A unit in a Treasury product

- A redemption right

- A digital ownership record

- Economic exposure to an asset

That list is important because beginners often assume too much.

A token linked to real estate may not give direct ownership of the property deed.

Gold-backed tokens may not give every holder instant access to a physical gold bar.

Private credit tokens may represent exposure to a loan pool rather than direct ownership of each loan.

The legal documents decide what the token means.

Marketing language does not.

This is where many weak products hide.

They use simple words like “backed by real assets” but avoid explaining the actual investor claim.

That is not clarity.

It is a warning sign.

RWAs vs Tokenized Assets

RWAs and tokenized assets are not exactly the same thing.

An RWA can exist without blockchain.

A house is still a real-world asset if nobody tokenizes it.

Government bonds are RWAs even when held through a normal brokerage account.

Fund shares can also exist through traditional records.

Once a digital token represents rights linked to that asset, it becomes a tokenized RWA product.

So the distinction is simple:

An RWA is the asset or claim.

A tokenized asset is the digital representation.

Do not blur the two.

Blurry language leads to bad investing decisions.

RWAs vs Crypto-Native Assets

RWAs are different from crypto-native assets.

A crypto-native asset exists directly on a blockchain network.

Bitcoin is the asset.

Ether is the asset.

A DeFi governance token usually belongs to a blockchain protocol.

RWAs point to something outside that system.

That creates extra dependencies.

An RWA token may rely on legal contracts, custodians, fund managers, property managers, auditors, banks, courts, or regulators.

None of that makes RWAs bad.

It simply changes the risk profile.

With RWAs, the bridge between the blockchain record and the real-world claim matters most.

If that bridge is weak, the token is weak.

Why Real Estate Is a Popular RWA

Real estate is one of the easiest RWA examples to understand.

Most people already understand property.

Buildings can produce income.

Property values can rise or fall.

Buying an entire property also takes serious capital.

That makes real estate a natural fit for fractional ownership and tokenization.

A real estate tokenization platform may divide exposure to a property into smaller shares, interests, or tokens.

Investors can then buy a smaller position instead of purchasing the whole asset.

The appeal is clear.

The risks are also real.

Tenants can leave.

Repairs can rise.

Local rules can change.

Property managers can perform badly.

Legal disputes can freeze cash flow.

Tokenization does not remove those problems.

It only changes how the investment is packaged, recorded, and transferred.

Why Treasuries Matter in the RWA Market

Tokenized Treasury products have become one of the strongest early RWA use cases.

That is not surprising.

Treasuries are familiar financial assets.

Pricing is easier to understand than many private assets.

Institutional demand already exists.

This makes Treasury-linked products easier to structure and explain.

For beginners, there is a useful lesson here.

The serious RWA market did not start with wild promises or strange assets.

A lot of early momentum came from boring financial products.

That is not a bad thing.

In finance, boring often means clearer rules, better pricing, and stronger trust.

Benefits of RWAs

RWAs can offer real benefits when the structure is strong.

The main ones are access, better records, faster transfers, and programmable rules.

Wider access

Tokenized RWA products may divide large assets into smaller units.

That can make some markets easier to enter.

Real estate is the obvious example.

A full property may cost hundreds of thousands of dollars.

A tokenized structure may allow investors to buy a smaller interest.

Still, smaller access does not make the product good.

A weak deal split into tiny pieces remains a weak deal.

Better records

Blockchain can help record ownership and transfers.

That may reduce manual work and improve tracking.

However, on-chain records have limits.

A blockchain may show who holds a token.

It will not automatically show tenant problems, unpaid repairs, legal disputes, or poor custody.

Useful records are helpful.

They are not a replacement for due diligence.

Faster transfers

Some tokenized products may support faster transfers than traditional systems.

That can help with settlement and operational efficiency.

The benefit matters more for institutions than many retail investors realize.

Large firms care about how assets move between systems.

Speed can save time and reduce back-office friction.

Even so, speed only helps when the legal structure works.

Fast transfer of a weak claim is not progress.

Programmable rules

Smart contracts can automate certain rules.

Transfers, eligibility checks, compliance controls, and distributions may become easier to manage.

That sounds powerful.

It can be.

But code cannot fix a poor asset, unclear rights, or bad management.

Technology should support the structure.

It should not distract from it.

Risks of RWAs

RWAs carry real risks.

The asset may lose value.

Income may disappoint.

Liquidity may be poor.

Custody can fail.

Legal rights may be unclear.

Platforms can shut down.

Regulation may limit access or transfers.

A beginner should not panic because risks exist.

Every investment has risk.

The problem starts when people ignore them because the product has a blockchain label.

That is lazy.

The RWA label does not make an investment safe.

The structure does.

Liquidity Is Not Guaranteed

Liquidity is one of the biggest traps in RWA investing.

Many people assume tokenization makes assets easy to sell.

Sometimes it may help.

Often, it does not.

A token still needs buyers.

The platform may have a secondary market, but that does not prove demand exists.

Transfer rules may also limit who can buy the token.

In regulated products, only approved investors may be allowed to hold it.

Before buying, check the exit route.

Ask these questions:

- Is there an active secondary market?

- Who is allowed to buy the token?

- Are transfers restricted?

- How much trading actually happens?

- Can the issuer pause transfers?

- Is redemption available?

- What fees apply when selling?

If the answers are weak, treat the product as illiquid.

A sell button is not liquidity.

It is only a button.

What Beginners Should Check First

Before trusting any RWA product, slow down.

The basics matter more than the branding.

1. What asset sits behind the token?

Find out whether the product links to property, bonds, credit, commodities, fund shares, or something else.

Vague phrases like “real asset-backed” are not enough.

2. What does the token represent?

Check whether it represents equity, debt, fund shares, income rights, redemption rights, or economic exposure.

This decides what you actually own.

3. Who controls the asset?

For property, look for the legal owner.

For gold, check the custodian.

In fund products, find the manager and service providers.

Private credit requires borrower and loan documentation.

4. How do investors get paid?

Income needs a source.

It also needs clear deductions.

Fees, reserves, management costs, taxes, defaults, and delays can all affect payouts.

Gross income is not investor income.

5. Can investors sell?

Look for real liquidity.

Do not accept vague marketplace promises.

Trading volume, buyer demand, transfer rules, and redemption terms matter.

6. What happens if the platform fails?

This is the stress test.

If the website disappears, do investors still have enforceable rights?

Who controls records?

Where are the legal documents?

How would investors communicate with the issuer or asset manager?

Weak platforms struggle with these questions.

Serious ones answer them clearly.

Common Beginner Mistakes

Mistake 1: Thinking every RWA token is safe

RWAs are not automatically safe.

Safety depends on the asset, issuer, legal structure, custody, platform, regulation, and liquidity.

Mistake 2: Believing the token equals ownership

A token may represent many things.

Direct ownership is only one possible structure.

Mistake 3: Ignoring legal documents

The legal wrapper matters more than the website design.

Documents define rights.

Dashboards do not.

Mistake 4: Assuming liquidity

Tokenized does not mean easy to sell.

A marketplace with no buyers is not an exit.

Mistake 5: Treating all RWAs the same

A tokenized Treasury fund is not the same as tokenized real estate.

Private credit is not the same as gold.

Each category needs separate analysis.

Are RWAs Good for Beginners?

RWAs are useful for beginners to understand.

They show how blockchain can connect with real assets, financial products, and traditional markets.

As an investment, though, not every RWA product suits beginners.

Some are complex.

Others have limited liquidity.

Many include legal structures that require careful reading.

Certain products may only be open to accredited, qualified, or institutional investors.

Education should come first.

Learn the asset.

Check the claim.

Understand the structure.

Only then should anyone think about investing.

Final Thoughts

So, what are RWAs?

RWAs are real-world assets.

They include assets and claims from outside blockchain networks, such as real estate, Treasuries, money market funds, private credit, commodities, invoices, art, and fund shares.

In tokenization, these assets may be represented through digital tokens.

That can improve records, access, transfers, settlement, and compliance.

But the token is not the whole story.

The real value sits behind it.

Before trusting any RWA product, check the asset, legal structure, custodian, issuer, fees, restrictions, payouts, and exit options.

The RWA label may catch your attention.

The structure decides whether the product deserves your money.

FAQs

What does RWA mean?

RWA stands for real-world asset. It refers to an asset, right, or financial claim that exists outside blockchain networks.

What are examples of RWAs?

Examples include real estate, government bonds, money market funds, private credit, commodities, gold, invoices, art, carbon credits, and fund shares.

Are RWAs the same as crypto?

No. Crypto-native assets exist on blockchain networks. RWAs are linked to assets, claims, or rights outside the blockchain world.

What is RWA tokenization?

RWA tokenization means using blockchain-based tokens to represent rights, claims, shares, or exposure linked to real-world assets.

Do RWA tokens mean I own the asset directly?

Not always. Some tokens may represent ownership, but many represent fund shares, debt claims, income rights, company interests, or economic exposure.

Why are RWAs important?

RWAs may connect traditional finance with blockchain-based systems. They can support digital records, faster transfers, programmable rules, and new access models.

Are RWAs risky?

Yes. Risks include unclear legal rights, weak custody, poor liquidity, platform failure, bad management, falling asset values, and regulatory limits.

What should beginners check first?

Beginners should check what the token represents, who controls the asset, how payouts work, what fees apply, whether liquidity exists, and what happens if the platform fails.