Project Agora is no longer just an idea.

Central banks are now testing how tokenized deposits move across borders. The focus is simple. Faster settlement. Lower friction. More control.

At the same time, the wider tokenization market has grown fast. Real-world assets now sit at tens of billions in value. Tokenized treasuries lead the way.

So this is no longer a theory.

It is an early deployment.

That shift matters. It changes how we should view Project Agora. It is not about potential anymore. It is about execution.

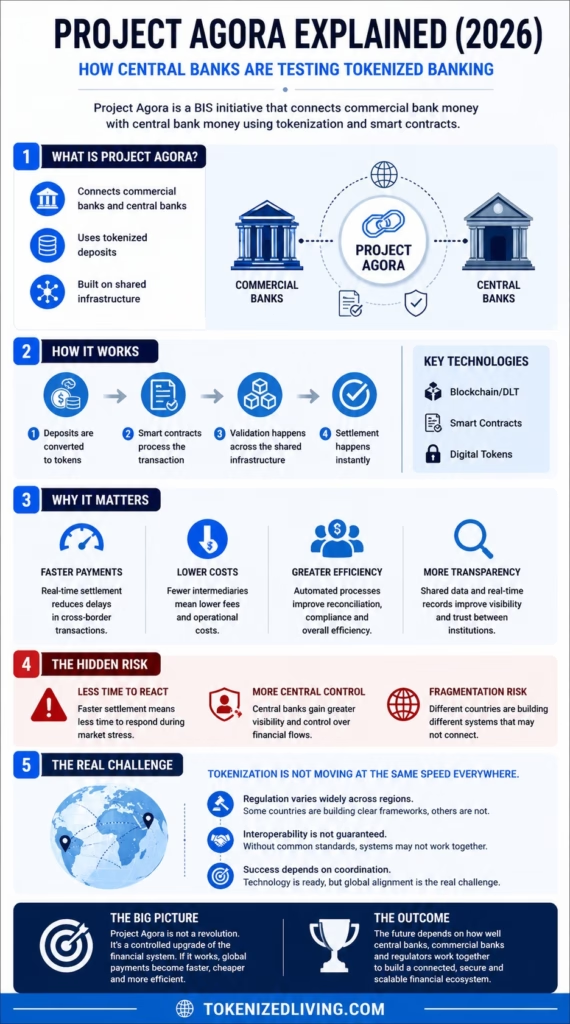

What Is Project Agora?

Project Agora is led by the Bank for International Settlements.

Its goal is to connect commercial bank money with central bank money using tokenization.

Today, these systems operate separately. Payments move through layers of intermediaries. That creates delays, cost, and complexity.

Project Agora tries to fix that.

It turns deposits into digital tokens. It then allows those tokens to move across a shared system.

If successful, banks could settle transactions faster and with fewer steps.

Where Tokenization Stands Today

Tokenization is moving faster than most expected.

The real-world asset market has already pushed into the tens of billions. Tokenized government bonds are leading that growth.

Institutions are not waiting around. Some platforms already handle billions in transactions using blockchain-based systems.

However, retail is still on the sidelines. That part has not caught up yet.

So there is a gap.

Infrastructure is improving quickly. Meanwhile, regulation is moving, but slower and uneven across regions.

That is where Project Agora fits.

Right between what is already working and what still needs to be aligned.

How Does Project Agora Work?

The idea behind Project Agora is simple.

Commercial bank deposits are turned into tokens. Central bank money is also represented digitally.

Once created, these tokens move on a shared infrastructure.

Instead of sending messages between banks and waiting for settlement, the transaction and settlement happen together.

As a result, delays are reduced.

It also cuts the need for reconciliation between systems.

Smart contracts play a role here. They automate parts of the process. For example, they can trigger payments when conditions are met.

So, instead of multiple steps, the system becomes more direct.

How Project Agora Compares to Other Systems

Project Agora is not the only system exploring tokenized finance.

Several models already exist.

| System | Focus | Key Difference |

|---|---|---|

| Project Agora | Central bank coordination | Settlement in central bank money |

| JPMorgan Onyx | Institutional payments | Private network model |

| mBridge | Cross-border CBDC | Strong Asia focus |

| Stablecoin systems | Open blockchain payments | Less central control |

The key difference is control.

Project Agora keeps central banks at the center. Other systems move faster but rely more on private infrastructure.

Ultimately, that trade-off will shape how tokenization develops.

Tokenization: A Shift Inside Banking

Project Agora tries to connect two systems that rarely meet.

On one side, commercial bank deposits. On the other, central bank money.

Tokenization allows both to exist in the same environment.

If this works, payments could move faster. Cross-border transfers could become more direct.

There is also growing interest in tokenizing assets like government bonds and gold.

That signals something important.

This is not just about payments anymore. It is about how value moves through the financial system.

Revolutionizing Payment Systems with Smart Contracts

The current payment system is slow.

It depends on intermediaries and separate systems that need to communicate.

Project Agora reduces some of that friction.

Smart contracts can automate settlement. Transactions can complete faster.

This reduces cost. It can also improve transparency between institutions.

But speed changes the system.

Faster settlement means less time to react when something goes wrong.

Therefore, that trade-off matters.

The Hidden Risk Behind Tokenized Banking

Tokenization improves efficiency. But it also introduces new risks.

Faster systems can amplify problems.

If markets move quickly, there is less time to intervene. That could increase volatility during stress events.

Another issue is control.

Central banks remain at the center of Project Agora. That gives them more visibility over transactions.

Some see this as stability. Others see it as increased oversight.

Then there is fragmentation.

Different regions are building different systems. Without shared standards, these networks may struggle to connect.

So while the benefits are clear, the risks are real.

Why Tokenization Is Not Moving at the Same Speed Everywhere

Tokenization is not global. It is fragmented.

Some regions are building clear regulatory frameworks. Others are moving more slowly. Some are restricting tokenization entirely.

This creates uneven progress.

For a system like Project Agora, that matters.

Cross-border payments depend on coordination. If countries move at different speeds, integration becomes harder.

So the challenge is not just technology.

It is alignment between regulators, banks, and governments.

The Promise of Tokenization in Financial Digitalization

The Bank for International Settlements is pushing this forward.

Their goal is to connect payments, transfers, and transaction data in one system.

Today, banks rely on separate processes. That increases cost and slows everything down.

Tokenization changes that.

Smart contracts can link payments with instructions automatically. This reduces manual work and improves efficiency.

Moreover, processes like KYC and AML could become more streamlined on shared infrastructure.

That is where the real value sits.

But this system is not fully decentralized.

Central banks still control the core layer. Tokenization is being built inside existing structures, not outside them.

Navigating the Future of Tokenized Commercial Banking

Project Agora does not replace the current system.

It upgrades it.

Commercial banks still manage customers. Central banks still control the base layer.

However, the difference is how these layers connect.

Tokenization could make that connection faster and more direct.

But there are still open questions.

Firstly, scalability is one. Interoperability is another.

Furthermore, if systems cannot connect across regions, the benefits weaken.

So the outcome is not guaranteed.

It depends on coordination as much as technology.

Related Reading on Tokenized Living

If you want to go deeper into tokenization, these guides break it down further:

These show how tokenization already works beyond central banking systems.

Conclusion

Finally, Project Agora shows where banking is heading.

It is not a revolution. It is a controlled upgrade.

Tokenization is being tested at the highest level, but within clear limits.

If it works, payments become faster and more efficient.

If it fails, the system becomes fragmented.

Essentially, that is the real story.

FAQs About Project Agora

What is Project Agora in simple terms?

Project Agora is a central bank initiative testing how tokenized deposits can improve cross-border payments.

Is Project Agora live?

It is still in testing. However, real-world trials are already underway.

Does Project Agora use blockchain?

Yes. It uses distributed ledger technology to move value more efficiently between banks.

What is the main benefit?

Faster settlement with fewer intermediaries.

What is the biggest risk?

Speed and control. Faster systems may increase systemic risk, while central banks gain more oversight.

Finally, we refined and enhanced the article using ChatGPT.