Consensys asset tokenization is not about a single product.

Older articles often get this wrong.

Describing Consensys as mainly a staking platform is too narrow now.

The stronger story sits deeper in the stack.

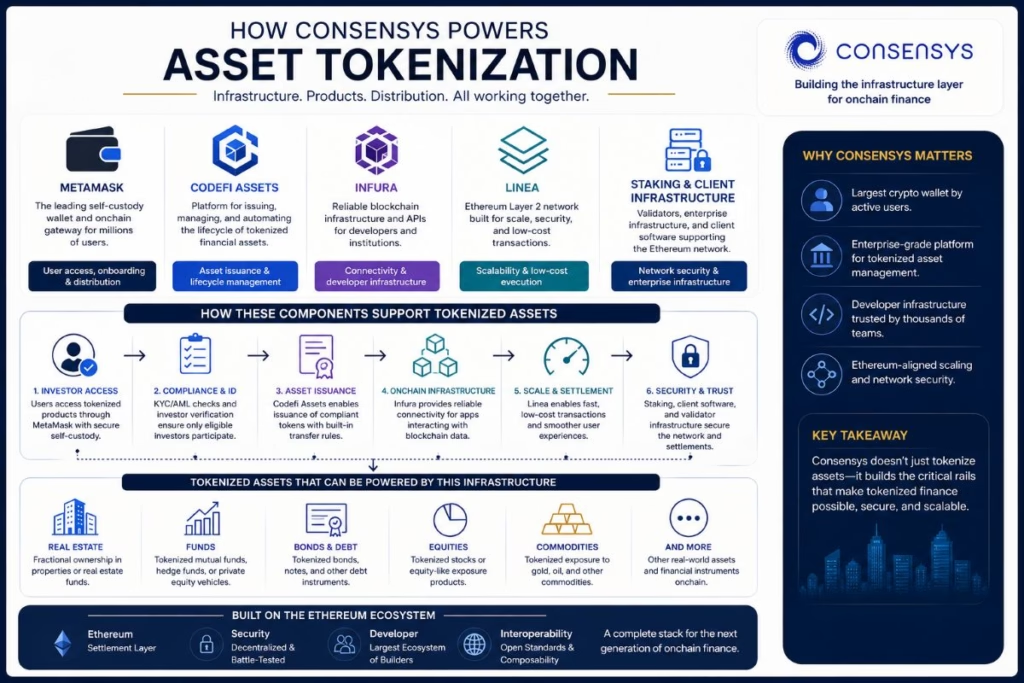

Through MetaMask, Codefi Assets, Infura, Linea, and Ethereum infrastructure, Consensys touches several parts of onchain finance. Some products face retail users. Others sit behind the apps investors use without ever seeing the name.

That mix matters because tokenization needs more than a smart contract.

A tokenized fund, real estate interest, stock product, or bond still needs investor onboarding, compliance rules, wallet access, blockchain connectivity, custody workflows, transfer restrictions, and clear legal rights.

Consensys is relevant because it operates near many of those rails.

The real question is not, “Does Consensys tokenize assets?”

A better question is this:

Could Consensys help power the infrastructure layer behind tokenized finance?

TL;DR

- Consensys is an Ethereum software and infrastructure company.

- Its tokenization role comes from MetaMask, Codefi Assets, Infura, Linea, staking tools, and Ethereum developer infrastructure.

- Codefi Assets is the clearest tokenization product in the Consensys ecosystem.

- Mata Capital used Consensys Codefi to tokenize real estate funds worth a combined €350 million.

- MetaMask now gives eligible users access to tokenized U.S. stocks, ETFs, and commodities through Ondo Global Markets.

- A tokenized stock or property product does not always mean direct ownership of the underlying asset.

- Consensys matters most as infrastructure, not as a normal tokenized real estate marketplace.

What Is Consensys?

Consensys is an Ethereum-focused blockchain software company.

Joseph Lubin, one of Ethereum’s co-founders, founded the company. Since then, it has become one of the better-known infrastructure names in the Ethereum ecosystem.

Most retail users know the company through MetaMask.

Developers may know it through Infura, Linea, Besu, Teku, or other Ethereum tools.

Institutions may look at Consensys through staking services, enterprise infrastructure, or Codefi Assets.

That range matters.

Consensys is not one clean product with one simple use case. It is closer to a group of tools sitting across the Ethereum economy.

For tokenization, the position is useful.

The company has wallet distribution through MetaMask. Developer infrastructure comes through Infura. Ethereum scaling comes through Linea. Digital asset issuance sits inside Codefi Assets.

Taken together, those products place Consensys near several layers of tokenized finance.

Why Consensys Matters to Asset Tokenization

Asset tokenization sounds simple until you look at the plumbing.

A basic explanation usually goes like this:

Take an asset. Create tokens. Let investors buy fractions.

Easy to understand, yes. Complete, no.

Real-world asset tokenization needs much more than a token.

A serious tokenized fund, bond, property interest, or stock-linked product needs rules. Someone must verify investors. Records need to be managed. Transfers may face restrictions. Payments have to be handled correctly. Custody must be clear. Legal rights need proper documentation.

Without those pieces, the token is just a shiny wrapper.

This is where Consensys becomes relevant.

MetaMask can act as the user gateway.

Infura can support applications behind the scenes.

Codefi Assets can help with asset issuance and lifecycle management.

Linea can give developers cheaper Ethereum-compatible execution.

Ethereum client software and staking tools support the wider network.

None of that makes Consensys a tokenized property marketplace. It does, however, make the company important to the infrastructure side of tokenized finance.

Older articles usually miss that angle.

Codefi Assets: The Direct Tokenization Link

Codefi Assets is the clearest tokenization product inside Consensys.

Calling Consensys mainly a staking platform misses the stronger point. Codefi Assets is built for digital asset tokenization, issuance, and lifecycle management.

In plain English, it helps institutions create and manage blockchain-based financial products.

Potential use cases include funds, bonds, debt instruments, private equity funds, special purpose vehicles, and asset management products.

Those assets do not behave like ordinary crypto tokens.

A tokenized fund may need transfer restrictions. Digital bonds may need investor records. Private equity products may only be available to certain investors. Real estate fund tokens may require KYC checks before anyone can receive them.

Codefi Assets is designed for that more complex world.

This matters because real-world asset tokenization often sits close to securities law. A serious tokenized asset usually needs compliance rules built into the process.

Launching a simple token and hoping liquidity appears is not enough.

For Consensys, Codefi Assets gives the company its most direct tokenization story.

How Consensys Helped Tokenize €350 Million in Real Estate Funds

The strongest example is Mata Capital.

Mata Capital, a French asset manager, partnered with Consensys Codefi to issue security tokens for three real estate funds worth a combined €350 million.

One project involved a logistics platform north of Paris worth €220 million.

That example gives the article real substance.

Instead of making vague claims about blockchain “transparency,” it shows how Consensys technology has already been used in institutional real estate tokenization.

The important detail is the structure.

Codefi Assets was not just used to create tokens. The project also included compliance requirements, KYC validation, and verified investor access.

That is how serious tokenization normally works.

A property does not magically become investable because someone creates a token. Legal structure, investor checks, and asset administration still matter.

For Tokenized Living readers, the takeaway is clear:

Consensys is not a tokenized real estate marketplace, but its technology has supported real estate fund tokenization at institutional scale.

That difference matters.

RealT, Lofty, and Reental sit closer to the investor-facing property platform layer.

Consensys sits closer to the infrastructure layer.

MetaMask and the RWA Gateway

MetaMask is the part of Consensys most people actually see.

For years, users treated MetaMask as a crypto wallet. It helped them store tokens, connect to decentralized apps, and manage Ethereum-based assets.

Now, MetaMask is moving closer to tokenized traditional finance.

In February 2026, MetaMask announced an integration with Ondo Global Markets. Eligible users in supported non-U.S. jurisdictions can access more than 200 tokenized U.S. stocks, ETFs, and commodities through MetaMask.

That includes tokenized exposure to stocks, ETFs, gold, and silver.

The move is significant for wallet-based finance.

MetaMask is no longer only a gateway to crypto-native assets. It is becoming a front door for tokenized financial exposure.

Still, the wording needs care.

A tokenized stock product is not always the same as owning the underlying stock directly.

Legal structure decides what the investor really holds.

Ownership rights can affect voting, dividends, redemption options, custody arrangements, issuer risk, and claims if something goes wrong.

So the MetaMask and Ondo integration matters, but it should not be hyped like a magic bridge between Wall Street and crypto.

The better takeaway is this:

MetaMask is becoming a distribution layer for tokenized financial exposure, not a guarantee of direct ownership.

That is the real story.

Legal Risk Box: A Token Is Not Always the Asset

Tokenized assets can give investors access to real-world value.

Access does not always mean direct ownership.

A token may represent a fund interest, contractual claim, receipt, debt instrument, synthetic position, or exposure to an underlying asset.

That distinction matters.

Before using any tokenized asset platform, investors should check:

- who issued the token

- where the issuer is based

- what legal rights the token holder has

- whether redemption is possible

- who holds the underlying asset

- how custody works

- whether transfers are restricted

- what happens if the platform fails

- whether the product is available in their jurisdiction

This is especially important with tokenized securities.

A token linked to a stock is not always the same as owning the stock. Property tokens are not always equivalent to holding the deed. Fund tokens may also represent interests in a vehicle rather than direct ownership of the assets inside it.

That warning should not scare people away from tokenization.

It should push them to read the structure properly.

Where Infura Fits Into Tokenized Finance

Infura is not the exciting part of Consensys.

Still, it may be one of the most important.

Developers use Infura to connect applications to Ethereum and other blockchain networks. Instead of running their own infrastructure from scratch, they can use Infura to read blockchain data, send transactions, and support Web3 applications.

Tokenized finance needs that kind of reliability.

Investor dashboards, transfer records, payment systems, fund platforms, and trading interfaces all need dependable blockchain connectivity.

When infrastructure breaks, users feel it quickly.

Transactions fail. Apps slow down. Records do not update. Confidence drops.

That is why Infura matters.

Most investors will never talk about it. Many will never know it exists. Yet the applications they use may depend on services like it.

This is a recurring theme with Consensys.

The company’s role is often not glamorous.

It is infrastructural.

Where Linea Fits

Linea is Consensys’ Ethereum Layer 2 network.

Its role in asset tokenization is still developing, so this section needs restraint.

Ethereum mainnet can become expensive during busy periods. That creates problems for tokenized finance, especially if investors expect smooth transfers, lower fees, and faster interaction.

Layer 2 networks aim to reduce some of that friction.

Linea gives developers an Ethereum-compatible environment with lower-cost execution. In theory, that could help tokenized finance products scale.

However, Linea should not be oversold here.

It is not the main reason Consensys matters to tokenization today. Codefi Assets and MetaMask are more direct.

A fair reading is simple:

If more tokenized finance activity moves through Ethereum-based systems, networks like Linea may help make those products easier and cheaper to use.

That is enough.

No need to dress it up.

The SEC Case and Why It Matters

Regulation belongs in this article.

Ignoring it would be sloppy.

In 2024, the U.S. Securities and Exchange Commission charged Consensys over MetaMask Staking and MetaMask Swaps. The SEC alleged that Consensys had engaged in unregistered securities activity through staking and had operated as an unregistered broker through MetaMask Swaps and MetaMask Staking.

This case mattered because it sat right where wallet software, staking, swaps, and securities law overlap.

In 2025, Consensys said it had reached an agreement in principle with the SEC for the MetaMask enforcement case to be dismissed. The SEC later announced dismissal of the civil enforcement action with prejudice.

That does not end every regulatory question around tokenized finance.

It does show how quickly legal pressure can reach infrastructure companies.

Investors should remember that point.

Tokenization is not just a technology trend. It sits inside a legal system that changes by country, product type, asset class, and investor category.

A clean wallet interface does not explain the full legal position.

The legal wrapper still matters.

Consensys Consensys asset tokenization vs Tokenized Real Estate Platforms

Consensys should not be compared directly with RealT, Lofty, or Reental.

That comparison creates confusion.

RealT and Lofty are investor-facing tokenized property platforms. Reental offers access to real estate-backed investment opportunities. These companies sit close to the product layer.

Consensys sits closer to the infrastructure layer.

Here is the cleaner breakdown:

| Category | Examples | Main Role |

|---|---|---|

| Tokenized real estate platforms | RealT, Lofty, Reental | Offer property-linked investment products |

| RWA product issuers | Ondo, Securitize, Centrifuge | Issue or manage tokenized financial products |

| Infrastructure providers | Consensys, Chainlink, Fireblocks | Provide wallets, data, custody, compliance, or network tools |

| Blockchain networks | Ethereum, Polygon, Avalanche, Solana | Provide settlement or execution layers |

This is the right way to frame Consensys.

It is not the company selling you a fractional apartment.

Its value comes from the rails behind the market.

That may sound less exciting, but it could be more important over time.

Market Insight: Infrastructure May Matter More Than the Asset

Most people judge tokenization by the asset in front of them.

Fractional property sounds simple. Tokenized funds feel familiar. Stock-linked tokens look closer to traditional investing. Gold-backed tokens are easy to understand because investors already know the asset.

The harder question sits underneath all of that:

Who controls the infrastructure?

Tokenized finance needs wallets, compliance systems, developer APIs, custody tools, smart contracts, identity checks, settlement networks, and asset administration tools.

Without those pieces, the asset itself does not move very far.

This is why Consensys deserves attention.

MetaMask gives it distribution.

Infura gives it developer reach.

Codefi Assets gives it a direct tokenization product.

Linea gives it Ethereum scaling infrastructure.

That combination is hard to ignore.

Consensys may not be the loudest name in real-world asset tokenization. Still, it has a credible claim to being one of the companies building the rails around it.

The Main Risks of Consensys asset tokenization

Consensys has a strong position, but the risks are real.

First, tokenization remains fragmented.

Different platforms use different chains, custodians, issuers, legal structures, and investor rules. That makes the market harder to understand.

Second, regulation can change quickly.

The SEC case may have ended, but tokenized securities, staking, swaps, and self-custodial interfaces still raise legal questions in many markets.

Third, wallet-based finance can confuse users.

When crypto tokens, stablecoins, tokenized stocks, funds, and commodities all appear inside one app, users may assume everything carries the same rights.

That assumption is dangerous.

Fourth, infrastructure does not guarantee adoption.

Strong tools do not automatically create liquidity, investor trust, or institutional demand.

Finally, self-custody creates responsibility.

MetaMask gives users control. Control also brings risk. Lost keys, phishing links, malicious approvals, and wallet mistakes can still lead to serious losses.

None of these issues destroy the Consensys story.

They make the story more realistic.

Final Verdict: Why Consensys asset tokenization Matters

Consensys is not easy to explain because it does not fit into one box.

A simple “staking platform” label misses the point.

So does calling it only the company behind MetaMask.

Its real importance comes from infrastructure.

MetaMask gives users access to onchain assets. Infura supports developers. Codefi Assets helps institutions issue and manage digital assets. Linea provides Ethereum-compatible scaling. Staking services and Ethereum client software support the wider network.

Together, those products place Consensys near several layers of tokenized finance.

For investors, the key point is simple.

Consensys may not be the company selling the tokenized property, stock, or fund. It may instead help power the rails those products use.

Its position matters.

Still, the lazy version of the story should be avoided.

Tokenization is not magic. Direct ownership does not automatically come with a token. Wallet access does not remove legal risk. Slick interfaces rarely explain custody, redemption, transfer rules, or investor rights.

The better way to view Consensys is as part of the infrastructure behind the next phase of onchain finance.

That is where the real story sits.

FAQs

Is Consensys a tokenization company?

Consensys is not only a tokenization company. It is an Ethereum software and infrastructure company. However, Codefi Assets gives Consensys a direct connection to digital asset tokenization, issuance, and lifecycle management.

What is Codefi Assets?

Codefi Assets is a Consensys platform for creating, issuing, and managing digital assets and financial instruments. It can support products such as funds, bonds, debt instruments, private equity funds, and special purpose vehicles.

Has Consensys worked on real estate tokenization?

Yes. Mata Capital partnered with Consensys Codefi to issue security tokens for three real estate funds worth a combined €350 million.

How is MetaMask connected to RWAs?

MetaMask now gives eligible users in supported non-U.S. jurisdictions access to tokenized U.S. stocks, ETFs, and commodities through Ondo Global Markets.

Do MetaMask users own the underlying stocks directly?

Not always. Tokenized stock products may provide exposure to an asset without giving direct ownership of the underlying share. Investors should check the issuer, legal rights, custody structure, and redemption terms.

Is Consensys the same as RealT or Lofty?

No. RealT and Lofty are investor-facing tokenized real estate platforms. Consensys is better understood as an infrastructure company with tools that can support tokenized finance.

Why does Consensys matter for real-world asset tokenization?

Tokenized assets need infrastructure. Wallets, developer tools, smart contracts, compliance systems, scaling networks, and lifecycle management all play a role. Consensys touches several of those layers.

Finally, we refined and enhanced the article using ChatGPT.